You could say thank heavens they have finally stopped buying the "dip". Then again, there apparently aren't any left!

That's the case, anyway, even if your notion of a "dip" is any day the market doesn't go up. So far there has been exactly one such occasion during 2018. Or worse still, if you assume the traditional metric of at least a 5% drop, you have already been out of the dip buying business for a lifetime---- whether measured in market lives or even dog years.

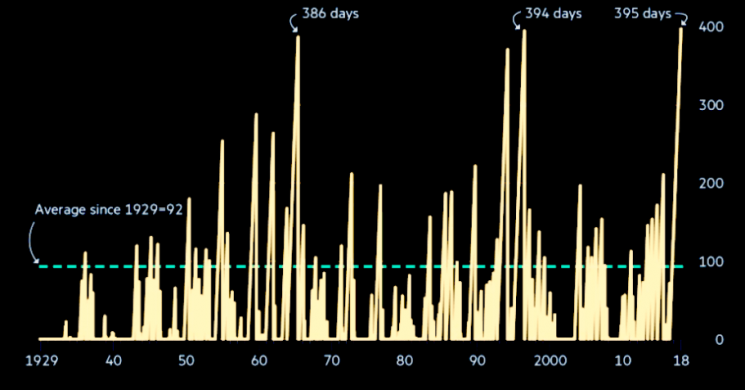

That's right. Heisenberg reminds us this morning that we are in undisputable record territory. It has been fully 395 trading days since the market had a 5% drop, and that's never happened before in all of recorded history.

Than again, the central banks of the world had never even dreamed of snatching $22 trillion of fiat credit from thin air prior to 1995, either. But in the nine years since the financial crisis they generated $14 trillion of new footings, and more than $20 trillion during the last three bubble cycles combined.

Needless to say, this $20 trillion emission of something for nothing has deformed and poisoned the entire warp and woof of the global financial system. Everywhere financial asset prices have been massively inflated and falsified, causing a two-phase distortion of the global economy.

Initially, massive money printing by the Fed fostered defensive currency market interventions (i.e. "dirty floats") and exchange rate suppression by the PBOC, BOJ, BOK and other exporters of both commodities and industrial goods. Buying in dollars to sequester in their own central banks, the mercantilist exporters of the world---including the dollar-linked petro-states---essentially imported the US dollar inflation.

So doing, of course, they expanded their own monetary bases and domestic credit systems with reckless abandon. That led, in turn, to a monumental global CapEx boom funded not by real money savings, but directly and indirectly by the prodigious fiat credit emissions of the mercantilist central banks. Accordingly, capital spending by worldwide publicly traded firms increased by 5X during the decade ending in 2012.

Ultimately that tsunami of cheap capital funded monumental excess capacity in global mining, energy, shipping, manufacturing and distribution industries and mobilized hundreds of millions of subsistence workers from the rice paddies and village economies of Asia into the globally traded markets. The resulting China Price for goods and India Price for internet based services, in turn, resulted in a massive flattening of the global labor cost curve.

Together, excess industrial and labor capacity ushered in an era of global commodity and industrial price disinflation that led to an utterly perverse reaction function among the Keynesian central bankers. That is, the only lesson they ever learned after the last remnant of real money was destroyed when Nixon trashed the Bretton Woods gold-exchange standard at Camp David in August 1971 is that too much monetary expansion leads to a rising and ultimately punishing CPI.

But the central bankers have not seen much CPI inflation in the present money printing era---especially after authorities sawed off the inflation ruler in the 1980s and 1990s via statistical tricks such as hedonics, geometric mean adjustments and imputations like homeowners equivalent rents in lieu of actual, measurable housing prices. So they perceived a green light to print central bank credit at will.

Except that was a gigantic mistake owing, ironically, to the fact that their mental models traced back to the hopeless economic nationalism and autarchic views of the Great Thinker himself, John Maynard Keynes.

After 1930 and long before his opus was published in 1936, in fact, Keynes had become a militant protectionist who advocated "homespun goods" and a thorough-going mercantilism that would make even Donald Trump blush.

Alas, Keynesian mercantilism doesn't work in an environment of global monetary expansion and billowing excess capacity and malinvestment. What transpired after the mid-1990s was, in fact, something new under the monetary sun that reduced the models of the Great Thinker and his American disciples to economic gibberish.

What we mean here is that in the pre-1971 world of gold-based money and relatively fixed exchange rates, to speak of CPI inflation was essentially to speak of "inflation in one country". That's because inordinate monetary expansion in that context led to excess demand, rising domestic wages, prices and costs and a surge of imports to fill the gap.

Alas, that was also the skunk in the woodpile. The counterpart of a swelling current account deficit was eventually an outflow of the settlement asset---gold---as foreign investors lost interest in accumulating the domestic currency liabilities of inflating countries.

At length, the loss of gold drained the inflating country's domestic banking system of reserves---- causing credit and domestic economic activity to contract, thereby squelching "inflation in one country".

Nixon's monetary jail break at Camp David in 1971 was precisely motivated by his desire to break the financial discipline of even the US dominated and wobbly gold exchange standard of Bretton Woods. That is, the required shrinkage of domestic credit to stem the demand for gold by other central banks sitting on mountains of dollar liabilities would have triggered a 1972 recession---and that Tricky Dick was not about to countenance.

In any event, globally synchronized money printing---especially after China elected to become a mercantilist exporter in the early 1990's under Mr. Deng's dispensation that it is glorious to be rich---- meant the opposite of what was implied by the bathtub economics of the Keynesian central bankers.

To wit, too much money printing in a globally-linked central banking system leads to excess capacity, rampant malinvestment and, consequently, industrial and consumer disinflation, not inflation.

That proposition became especially apt after the global CapEx and commodity peak of 2012. Thereupon the massive emission of central bank credit has simply swirled in the canyons of Wall Street and its counterparts in the global financial pool.

That is, it lead to a virulent financial asset inflation that the Keynesian central bankers could not recognize---- even when it smacked them in the face. On the eve of the last cycle, for example, it was evident that the price of mortgage backed securities---especially those backed by subprime loans--had reached insane levels, thereby fueling a virulent inflation of residential housing prices that was completely detached from the fundamentals of household income and ability to pay.

Likewise, today the Russell 2000 sits at 1600, which represent a preposterous 135X reported earnings of the small and mid-sized main street companies which comprise the index. Yet the most central bankers can muster in the face of that sheer insanity is that stock prices have become slightly "elevated".

No they haven't. They have shot the moon and then some. And now the indices continue to melt-higher only because the massive sea of restless liquidity that has been generated by the central banks over the last two decades is financing a level of speculation and momentum based trading---- by carbon and silicon based units alike--- that has no precedent in all of recorded history.

Alas, the present momentum-driven insanity is, mercifully, the last gasp of the Keynesian central baking era. The $22 trillion of central bank credit outstanding is the high water mark. Someday it will be recorded by historians that the turning point in modern economic history occurred when the central banks pivoted to QT under the mistaken conclusion that they had delivered the nirvana of Full Employment to main street.

No they haven't. There are 43 million food stamp recipients, 102 million adults without jobs (of which only 50 million are 65 or older), stagnant real wages, 30% lower real median household net worth (since the late 1990s), and $67 trillion of public and private debt outstanding which all suggest otherwise.

Moreover, the entire edifice of inflated financial assets is predicated on ultra-low interest rates essentially forever and an endless business cycle expansion, world without end.

But that's not going to happen as the central banks move into QT, led by the Fed's plan to dump bonds from its balance sheet at a $600 billion rate come October. And not surprisingly, the bond market is slowly arousing from its slumber owing to that prospect.

As Heisenberg further noted this morning, the best start in history by the stock market has been coupled with the worst start for the bond market:

...... bonds have gotten off to an abysmal start, with 10Y Treasurys posting their worst performance through January 19th in history as yields spike amid jitters on global demand (e.g. China) and questions about what the ballooning deficit will entail for Treasury’s borrowing needs (i.e. increased supply at a time when the Fed is stepping away from the market):

And this brings us to the real evil of Bubble Finance, which we will elaborate upon in Part 2. Namely, it not only leads to bubble crashes and speculators getting the painful deserts they fully deserve; it also destroys all the pricing signals that are essential to financial discipline on both ends of the Acela Corridor.

Consider two illustrations, which are only the tip of the iceberg. On the one hand, the Imperial City has been so fiscally euthanized by cheap interest rates and central bank absorption of the public debt that is has now thrown every semblance of caution to the winds.

In passing yesterday's 16-day can kick on the CR, it loaded on a two-year deferral of the ObamaCare taxes on Cadillac plans, insurance companies and medical devices.

That is scored as a $31 billion revenue loss, but in truth it is the third time these taxes have been deferred, meaning that are never meant to be collected. The true revenue cost is upwards of $310 billion over a decade. And that's on top of what is already heading for $15 trillion to $20 trillion of new deficits owing to the baseline policies and the tax cutting and spending sprees of the Trumpite/GOP underway.

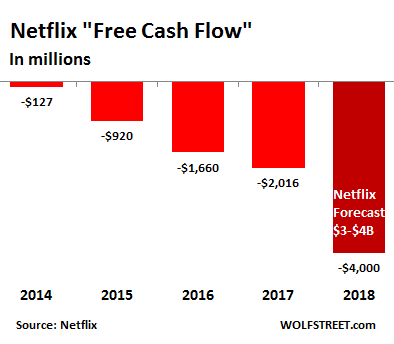

Likewise, it now appears that Netflix will generate operating free cash flow of almost negative $9 billion over the five years ending in 2018. Yet its market cap has soared to $110 billion based on pure speculative momentum.

Indeed, the whole world of media and tech is piling into streaming services and orginal content production, meaning that there is no possible way of knowing whether Netflix will ultimately generate a profit even remotely commensurate with its bloated valuation.

What is clear, however, is that the $10 billion it has borrowed at rock-bottom junk bond rates to fund its prodigious cash burn is not even remotely rational or sustainable.

Read more by MarketSlant Editor