Via Adam English and Outsider Club

Signs of A Crash: Decadence and Complacency

Slowly, but surely, we're approaching a notable anniversary.

On October 12th, 2007, the markets hit a high mark that wouldn't be seen again for nearly six years. We're six months from the 10th anniversary of the peak before the 56% drop in the S&P 500.

Soon, we'll be remembering the cascade of portentous events through news headlines and retrospectives, only now with a smugness that hindsight and distance allow us to afford.

With these headlines will come talk of the lessons hard learned. Mentions of those left behind in the pyrrhic victory that eventually allowed those left standing to rise to new heights will be made, but they'll almost entirely be in the past tense.

As if all the damage done back then ended back then as well. As if so many aren't still living in a constantly evolving struggle of diminished fortunes and fates. As if what doesn't kill you always makes you stronger.

After all, we so rarely can stomach a story without a silver lining, or a neat and tidy ending. Loss without any gain only lets that nagging voice in the back of our minds ask us, “what was the point?”

No wonder so many of those with influence or power have failed to ask these questions: Did we learn the right lessons? Have we truly put our flaws behind us? Did we find a point to so much suffering?

It was a chaotic and dirty affair, and one that we found too painful and bleak to address then through now. We can certainly see that today with so many protagonists absolved of all crimes, if not rewarded in the end.

It feels better to let ourselves believe that we got it right, and sweep it under the rug, then continue to reopen old wounds, and feel vulnerable.

That alone should give us pause. What we are seeing today in the markets should truly make us worry.

We may not face the same type of calamity in the markets or economy, but we certainly see some of the same underlying causes — decadence and complacency — guiding us toward another crash.

The Decadence of Companies

We're coasting through a period of decadence in corporate America that is nearly unprecedented in recent history.

The Great Recession was ushered in through vast swaths of the country living far beyond their means, and a financial sector more than willing to cater to it while adding layer upon layer to it.

We see some of that today through a complete removal of risk being priced into debt and questionable lending, but we're seeing a much larger part of the market create the same risks on their own balance sheets.

We've seen horribly repressed investment in the future through low capital expenditures, and the funds that would fuel tomorrow's growth go into corporate debt and share buybacks.

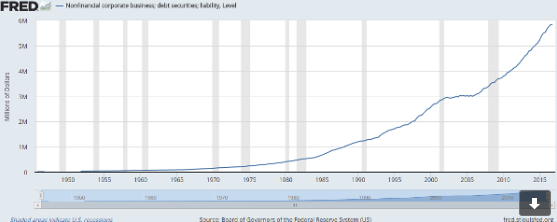

Corporate debt levels have never been higher. Though it may be supplied by the Fed and global QE, it is the corporations themselves who issue it.

And a disturbing level of that borrowing, which takes money from the future and pumps it into the market today, being routed into buybacks at or near all-time highs in share prices.

Record levels of share buybacks at these highly priced valuations are only bound to continue. Though the end of last year saw share buybacks fall off, all signs point to a renewed influx.

Both Citibank and Goldman Sachs research point to share buybacks hitting a level of total corporate cash not seen since 2007.

Goldman expects that total capital usage will increase by 12% to $2.6 trillion with 52% allocated to investing for growth (capex, R&D, and cash M&A) and 48% to returning to shareholders.

The only other time 48% of total cash was returned to investors was back in 2007 just ahead of the bursting of the credit bubble.

At the same time, corporate America is spending far more to fuel mergers and acquisitions than it should.

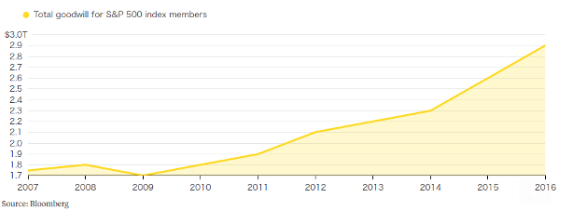

Goodwill — the difference between what assets are worth on paper and how much an acquirer paid for them — is also soaring. At S&P 500 companies, goodwill has risen by two-thirds over the past decade and accounts for more than one-third of net assets.

In the past two years, takeover targets have sold for a median of 11 times earnings, before interest, taxes, debt, and amortization. That is essentially 11 years of profit paid as a premium, with interest from the debt that funds the deals tagged on to boot.

The multiple was only about 7 to 9 times in the years leading up to the recent merger frenzy.

Earnings will suffer, especially with any pullback in share prices and the write-downs that will result. Assets on paper will vanish, along with profits on paper for investors.

The Complacency of Markets

While corporations and their executives are living in decadence, beyond the means that their companies can fundamentally support, the markets and investors are complacently playing along.

Homeowner debt is rising, and credit card debt has passed the $1 trillion mark again for the first time since the Great Recession. Hardly good signs when consumption stands at a record 69.4% of gross domestic product.

Consumer confidence is strong on paper, but the bills will always come due. Rising delinquency and default rates are already here.

While these consumers load up on debt, they allow the corporations they invest in to do the same. And make no mistake, this credit and corporate debt are fueled by investors. Credit expansion is almost entirely limited to the middle class and up.

People are borrowing more in the belief that the money in their retirement accounts is the same as real money, in spite of the fact that it can disappear overnight.

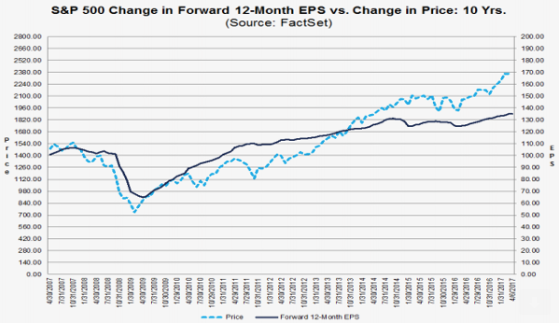

Along with the risks from goodwill and from overall corporate debt, share prices have soared far beyond earnings.

The levels we're seeing would take far too long for tepid earnings growth, and weak economic growth, to catch up in any reasonable time.

At current levels, the market is vulnerable to a crash for years to come.

Heed the Warnings

Going on 10 years since the Great Recession, it is very clear that corporations, the market, politicians, and investors have all dropped their guard.

Many who weren't ruined and faded into obscurity last time around have fallen into the decadence that seemingly risk-free debt can give them at the cost of tomorrow's earnings, or become complacent to ride along until the bitter end.

I am far from alone in this view. The warning calls have been coming from more and more people, and now one of the most legendary outsider investors is weighing in as well.

James Dines is one of the biggest names in financial publishing. When Wall Street didn't believe him, he was fired.

But Mr. Dines stuck to his guns. And he decided to take his message public. So he warned the world of the coming gold boom through his own newsletter.

It was the first newsletter to be published independently outside of a Wall Street brokerage firm or bank.

And it was Mr. Dines and his readers who ultimately got the last laugh. His $400 gold call looked conservative when gold hit $850.

The Internet stock boom in 1996, the dot-com bust in 1999, the second wave of gold and silver bull market in 2001, the rise of China, the housing collapse in 2007, and current deflation. He was ahead of all of them.

Don't be complacent. Folks who are willing to make investment calls in the face of the harshest criticism and defiance from the powers-that-be are rare. Read what this legend has to say.

Read more by The Hound