Treasury auctions.

via Matt Levine

Maybe Banks Manipulated Treasury Bonds, Too

Or maybe they didn't. You need to see some chats to be sure.One thing we've learned since the financial crisis is that banks like to get together and rig things. At the very least, they got together and rigged Libor and some foreign exchange fixes. 1 We know this pretty definitively because there are tons and tons and tons of e-mails and electronic chats in which bank traders talked with each other about manipulating Libor and foreign exchange rates. The FX chat rooms even have names like "the Cartel." You read the chats, and you know something bad was going on.

Which is useful, because another thing that one could, with careful attention, have learned since the financial crisis is that it can be tricky to separate illegal manipulation from legal but awkward-sounding activities. So Libor. Libor manipulation consisted of making up arbitrary numbers and passing them off as the interest rate at which banks could borrow. But Libor consisted of making up fake numbers and passing them off as the interest rate at which banks could borrow. 2The difference is that Libor manipulation consisted of intentionally skewing the numbers to make a bank look better or to make its derivative trading more profitable. If you didn't have the chats, you'd have a hard time distinguishing the manipulated numbers from the perfectly fine made-up numbers.

Or FX. In FX manipulation, traders took customer orders to buy currencies at a specified fixing time and then bought those currencies ahead of the fixing time, pushing up the price and allowing the banks to sell the currencies back to the customers at a higher fixing price. That sounds awful, when you say it like that. But that was actually fine! 3 That was so fine that shortly after the big FX settlements the banks sent letters to their clients reminding them that it was fine. What wasn't fine was that the traders also shared the customer orders with each other in chat rooms with dumb names. This made it a bit easier for the banks to push up the price, though it probably didn't make it that much easier, and the banks probably didn't make much money doing it, particularly not compared with the fines. Still, it was obviously bad behavior, as you can tell from the chats.

It seems quite plausible that the next round of big banks-rigging-things cases will be about rigging the Treasury auction market. And it seems quite likely that those cases will look a lot like Libor and FX. "As U.S. Probes $12.7 Trillion Treasury Market, Trader Talk Is a Good Place to Start," is this Bloomberg headline, and quite sensibly! It is always a good place to start, and one assumes that the Justice Department started there.

But the way the world works is that, as soon as the world finds out that the Justice Department is investigating a banks-rigging-things case, a lot of private plaintiffs' lawyers launch lawsuits against the banks, hoping for a piece of the action. "For shareholder lawyers, Treasury auction antitrust case is next big thing," is this Reuters headline, and quite sensibly! There's a lot of money in the Treasury market, and if the Justice Department is looking at it, then the chats are likely to be quite juicy.

But the plaintiffs' lawyers don't have the chats yet. 4 So they have to fall back on public evidence. And the way they do that is kind of weird.

Here's one of the main investor lawsuits, brought last month against a group of primary-dealer banks on behalf of plaintiffs including the Cleveland Bakers and Teamsters Pension Fund. 5 Here's a Bloomberg article about the plaintiffs' analysis. Here's how I would summarize the analysis, schematically:

- Banks made money on Treasury auctions.

- Remember all those other things they manipulated?

Point 2 is, of course, a fair point, and the complaint devotes nine pages to it. 6 The syllogism "banks manipulated things; this is a thing; therefore banks manipulated this" is not airtight, exactly, but it has a certain inductive appeal.

But I want to focus on point 1. The entirety of the plaintiffs' evidence of manipulation here is that the banks made a profit from participating in Treasury auctions that is statistically distinguishable from zero. So, for instance, the plaintiffs look at auctions of Treasury re-issues, in which the Treasury auctions new bonds that are interchangeable with existing bonds that are already trading in the secondary market. Here's the complaint:

On certain occasions the Treasury re-issues the same exact securities in a follow-on auction. Again, because the promise to be paid a dollar by the Treasury, is a promise to be paid a dollar by the Treasury, yields in a competitive auction for re-issued Treasuries should be the same as yields for the same exact thing available on the secondary market.

That, again, is not what the data shows. Instead, again, Defendants were able to consistently secure for themselves—despite the purported confidential, competitive auction— windfall yields/bargain prices in the follow-on auction as compared to what was being demanded in the secondary market.

And: "Across all tenors, the auction yields of reissued Treasuries were inflated in 69% of auctions (i.e., Defendants got a bargain price 69% of the time), by 0.91 basis points." For instance, in the 10-year bond, 62.5 percent of reissuance auctions resulted in a higher yield (lower price) to the dealers than in the contemporaneous secondary market, with an average higher yield of 1.75 basis points. (For the current 10-year that works out to a price that is about 0.15 percent lower than the secondary-market price. 7 ) So, statistically, the primary dealer banks got a discount of let's just say about 0.15 percent when they bought new 10-year Treasuries at auction.

Is that because they conspired to drive down the auction price? Quite possibly! But it's worth noting that dealers are supposed to make money intermediating bonds. For instance, when banks underwrite corporate bonds, they buy those bonds from the issuer at a discount to the price at which they can sell them -- even if the issuer has a liquid benchmark bond complex for comparison. (Even if the issuer is reopening an existing bond!) This is in part to pay the banks for taking risk in the underwriting, in part to compensate the banks for the work of distributing the bonds to investors, and in part to compensate the banks for all the other free work that they provide to the issuer in the hopes of winning bond deals. All of those reasons are attenuated in Treasury auctions, where the risks are lower, the distribution is easier, and the relationship is more arm's-length. 8 Still, it would be weird if primary dealers distributed Treasuries for free. They are providing a service that the Treasury wants as part of an explicit relationship. Even when the Treasury is issuing bonds that are interchangeable with existing bonds, it should expect to pay some (implicit) intermediation fee to get those new bonds into the hands of investors.

Now the 0.15 percent discount that the plaintiffs assert the banks get on new 10-years does seem, to my untutored eye, kind of high. Some comparisons: When Apple did a 10-year bond earlier this year, the banks bought it at a 0.60 percent discount, four times as big as the alleged discount here. 9 But underwriting a corporate bond offering is a lot harder and riskier than participating in a Treasury auction, and you'd expect the Treasury to get a significantly better deal than Apple. Another way to compare is that the bid/ask spread on the 10-year Treasury typically runs a bit more than 1/64 of a point; a bank trading Treasuries in the secondary market would earn about 0.017 percent per trade, an order of magnitude less than the banks allegedly made on these auction trades. But of course primary underwriting generally is more expensive than secondary-market trading.

The point, though, is that the plaintiffs here don't exactly argue that the banks made a bigger profit than they should have on intermediating Treasury auctions. Rather they say that the banks should have made zero expected profit, and made more than that. Take another passage from the complaint, this one about auctions generally (not just of re-issued bonds):

If someone gets something in an auction for a truly bargain price, they should be able to turn and sell it for a profit. That is, in fact, what the data shows occurred. Defendants were, once again, anomalously and predictably “winners” in the auction. A disproportionate number of times, yields went down for the just-auctioned Securities following the auction (i.e., prices went up) over the course of the rest of the day, or the next one. The odds Defendants by random chance (and without collusion) secured a preferential auction rate across so many maturities, across so many auctions, is statistically zero.

But you hear the same things all the time about market makers in other markets. It is a perennial topic of complaint that electronic market-makers always make money. Certainly lots of people think that they make this money by cheating, but the more straightforward explanation is that they are in a market-making business, charging counterparties a bid/ask spread to provide liquidity. You may think they overcharge, but the relevant point is that if they couldn't reliably make money in that business, they wouldn't be in the business. If banks couldn't predictably make money bidding for Treasuries at auction, they wouldn't bid for Treasuries at auction. (Of course, they are required to bid for Treasuries at auction by virtue of their primary dealer status, but that's no objection. If you are bidding for something at auction only because you are required to, not because you want to, then you have every incentive to underbid. 10 )

Now you might argue, as the complaint does, that the only way to reliably bid less than the market price for Treasuries is by collusion. But the complaint itself refutes this. The plaintiffs have all sorts of ways of comparing the auction price to the contemporaneous fair market price. As we discussed, they compare auction and secondary prices of re-issued bonds, and subsequent trading prices of auctioned bonds; in both cases they find that the dealers paid less than the fair price for auctioned bonds. They also compare auction prices to the when-issued market, and find that "when-issued yields before the auction were consistently predicting lower yields than what occurred (i.e., they were guessing prices in the auction would be higher than they ended up being)." There is similar evidence from the futures market, and from the trading prices of similar but not identical on-the-run Treasuries.

The plaintiffs take this as evidence of manipulation. Maybe! But what it also shows is that, if you were a Treasury dealer, you could know what the fair price was. 11 After all, the plaintiffs claim to know what the fair price was, from lots of different evidence. But if you are a Treasury dealer, there is no reason to bid the fair price. Not because you're manipulating, but because you are an intermediary -- a dealer -- and the "right" price for you to bid is the fair mid-market price minus your fee for intermediation.

Of course, the fee for intermediation should be competitive, and in the absence of collusion you'd expect it to be competed down. But you wouldn't expect it to be competed down to zero. The U.S. equity market used to be very un-competitive, and the fee for intermediation was about 12.5 cents. Now it is very competitive, and the fee is about 1 cent, sometimes much less. But it is not -- statistically, in the long run -- zero. Intermediaries still get paid something. Electronic market-makers still, controversially, make money.

A daily take on Wall Street, finance, companies and stuff.

Matt Levine's Money Stuff

None of this means that the Treasury market wasn't manipulated. Really the purpose of this complaint is to fish for the chats: The idea is that if the complaint states a plausible claim for manipulation, the plaintiffs may get discovery, and may end up finding chats and e-mails that prove collusion and manipulation. And it's not an implausibleclaim: I suppose you could argue that those consistent profits are too high. The best evidence for that is probably that, as the complaint puts it, "Following the Announcement of the DOJ's Treasuries Investigation, Signs of Artificiality Dissipated," which sure is a suggestive clue that the banks might have been misbehaving and knocked it off as soon as the DOJ started inquiring. 12

Still, it is worth remembering that sometimes financial intermediaries are allowed, even expected, to make money. The system may in fact be rigged in a way that allows Treasury primary dealers to make a profit by bidding for Treasury bonds at auction. But that might just be how the system is supposed to work. We'll only know for sure when we see the chats.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

-

They rigged ISDAfix too. And there is widespread suspicion -- and a Justice Department investigation -- about metals-market rigging. (There is also a settled case of metals manipulation, by Barclays, but that is more about one guy's manipulation than a widespread conspiracy.)

-

I am constantly quoting the proposition that Libor was "the rate of interest at which big banks don't lend to each other." It was always a survey-based number, not a market rate, and so was always in some deep sense made up.

-

It was! The U.K. Financial Conduct Authority said:

A firm legitimately managing the risk arising from its net client orders at the fix rate may make a profit or a loss from its associated trading in the market. Such trading can potentially influence the fix rate. For example, a firm buying a large volume of currency in the market just before or during the fix may cause the fix rate to move higher. This gives rise to a potential conflict of interest between a firm and its clients.

And, again, I recommend Dan Davies on the subject.

-

It is much easier for the Justice Department to get them than it is for the plaintiffs' lawyers, not least because cheerful and enthusiastic cooperation with the government is the main way for banks to reduce the penalties that they ultimately pay. There's a policy and everything.

-

The lawyers on this case are led by Cohen Milstein Sellers & Toll PLLC and Quinn Emanuel Urquhart & Sullivan LLP. Alison Frankel lists this case firstamong those brought by "some of the most successful plaintiffs' firms in the business," though there are other complaints by other big firms. Also what do you think the meetings of bakers and teamsters are like?

-

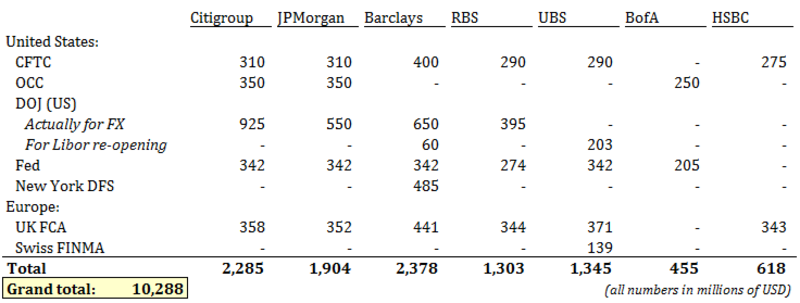

Pages 55-63, hitting high points including Libor, ISDAfix, FX and gold. Also a chunk of page 54 is devoted to Salomon Brothers' past manipulation of Treasury auctions.

-

That is, Bloomberg shows the 2 percent of August 2025 as having a dollar value per basis point ("DV01") of $877 per $1 million principal amount, so 1.75 basis points would be worth about $1,534 per million or about 0.1534 percent of par. The comparable number for the 30-year -- I see $1,928 of DV01, and the complaint alleges an average positive spread of 2.28 basis points -- is 0.44 percent. For the 26-week bill ($49.38 DV01, 0.74bps average spread), it's 0.00365 percent, or a bit under half a basis point of principal.

-

Though not non-existent. Primary dealers are expected to "provide the New York Fed’s trading desk with market commentary and market information and analysis helpful in the formulation and implementation of monetary policy," much like investment banks do for corporate clients.

-

Separately, investors who buy corporate bonds in new issues tend to make money. I think that the right way to conceptualize this is, again, that issuers are compensating the investors for taking a risk on a new bond. You might expect something similar to happen in the Treasury market, though of course on a much smaller scale because the risk is so much smaller.

-

This is I think the right way to interpret paragraphs 131 to 132 of the complaint:

As seen in the studies set forth in the preceding Sections, yields within the auction systematically departed from other measurables within the marketplace. Strikingly, when Defendants were more involved in a given auction, the observed anomalies were bigger. Conversely, when Defendants were less involved in a given auction, the observed anomalies were smaller. In other words, Defendants’ level of involvement in an auction, and the level of price artificiality went hand-in-hand.

This can be seen in the following chart, which uses a regression model to measure how correlated the amount of securities Defendants “won” in a given auction was, with respect to the size of the gap between the auction yields and the yields at the end of the auction day, after having controlled for contemporaneous market movements in the secondary market. The numbers are negative, for all the maturities. Which is to say, again, the more securities Defendants “won,” the more artificial (too high) the auction rate yields were.

But if your model is just that bank dealers (non-collusively) charge for providing liquidity, and fundamental-investor primary bidders do not, then the more primary bidders there are, the higher the price will be. If the only bidders for an auction are primary dealers who are required to bid, of course their bids won't be that aggressive. That's not collusion, it's just how auctions work.

-

Put another way, there's no reason to expect a "winner's curse" in the Treasury market, because there's lots of data on market values.

-

Though technically the claim is that they knocked it off as soon as the press reported that the DOJ was inquiring:

On June 8, 2015, media outlets first reported that the DOJ was investigating Defendants for their potential role in a conspiracy to manipulate Treasury auction yields. Even in the limited number of auctions since that time, a break in the pattern has emerged. With one lone exception, yields no longer retreated with the same speed they once did on auction days.

Read more Follow @matt_levine on Twitter

Read more by Soren K.Group