Appeals Court Overturns Dismissal in JP Morgan Silver Rigging Case

- US Appeals Court overturns Dismissal in Silver Rigging Case against JPMorgan

- The Appeals court rejected Judge Engelmeyer’s claim that the plaintiffs did not prove JPMorgan made “uneconomic bids” in the silver forward’s markets.

- New Discovery May Win the Case for against JPMorgan

Summary

The New York 2nd U.S. Circuit Court of Appeals ruled yesterday that District Court Judge Engelmayer was in error when he dismissed the Silver price rigging lawsuits against JP Morgan. The appellate court felt that Engelmayer’s dismissal reasons amounted to “impermissible fact finding” and placed too high of a bar in concluding that plaintiffs had not adequately plead their case.

This reversal of the June, 2016 dismissal means the case will go back to the district court for further litigation. This also means the plaintiffs will ask for and receive more discovery. This can win the case for them.

The Lawsuit Was Dismissed in June,2016

JPMorgan Chase & Co had won the dismissal of three private antitrust lawsuits, including from hedge fund manager Daniel Shak, accusing the largest U.S. bank of rigging a market for silver futures contracts traded on COMEX.The lawsuits accused JPMorgan of having in late 2010 and early 2011 placed artificial bids onto the trading floor, harangued employees at metals market COMEX to obtain prices it wanted, and made misrepresentations to a committee that set settlement prices.

- Our report June 30, 2016 JPM Silver Decision Flawed

Why it Was Dismissed in June

U.S. District Judge Paul Engelmayer in Manhattan, however, said the plaintiffs, who also included traders Mark Grumet and Thomas Wacker, did not show that JPMorgan made "uneconomic" bids, or intended to rig the market at counterparties' expense.

He also questioned the plaintiffs' use of Silver Indicative Forward Mid Rates ("SIFO") as a benchmark for determining proper levels for the spreads in their lawsuits.

In fact on April 21st, 2016 JP Morgan urged the judge quash the litigation. JPMorgan insisted allegations that the bank monopolized the market were too vague to support antitrust claims. They urged the judge ot raise the bar for the plaintiffs' burden of proof.

The Appeals Court Overturns the Dismissal Yesterday

The appellate court held that the plaintiffs did in fact submitted evidence that did in fact reach a level warranting further investigation. Therefore, the case should not have been dismissed.

In quoting the law, the 3 judges stated:

A plaintiff need only allege enough facts ‘to raise a right to relief above the speculative level,’ and ‘state a claim to relief that is plausible on its face.’

They stated that Judge Enlgemayer’s requirements for such specifics were too high to reach, describing the proof bar being raised to “a level of detail not required to withstand a motion to dismiss”

In essence what Judge Engelmeyer asked of the plaintiffs was impossible to ascertain in those proceedings.

Specifically: “Fact-specific questions cannot be resolved on the pleadings.”

Can JP Morgan Monopolize Silver? Yes

The appellate court noted that the plaintiffs' allegation of JP Morgan’s ability to control silver futures prices with reference to a particular market was proven correct. Thus,

"The District Court did not err in concluding that the Plaintiffs plausibly alleged a relevant market.”

This means that the plaintiffs showed plausibility that JP Morgan could control the far end of the Silver futures term structure via non-competitive bids.

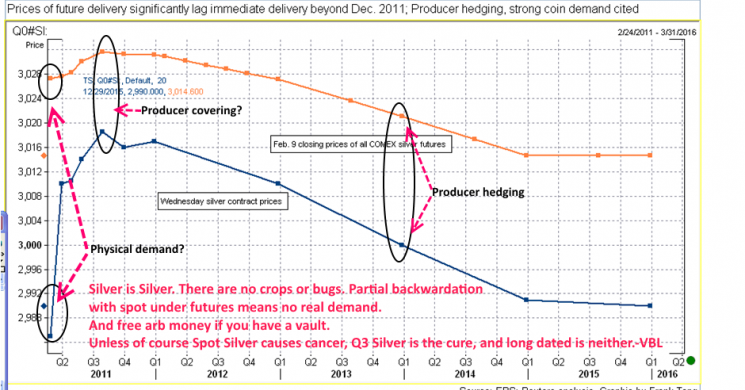

To traders, that means the JPM client who had to sell back month was faded way too low. [EDIT- And when one looks at the term structure from then, it is obvious that no true physical demand was in evidence based on the spot contango.- Vince Lanci]

Did JP Morgan Monopolize Silver? To be Determined

The Appeals court did not say they believed JP Morgan exercised such ability to monopolize the Silver market. But the statement that they noted the power to do so was proven in the first hearing is significant in that it agrees with the District court’s findings.

What Next

- The appellate court says the plaintiffs made a sufficient enough case for further investigation into a monopoly claim

- The findings of the appellate court will accompany the case file

- Judge Engelmeyer’s decision is removed and the case is remanded for further litigation and discovery

MarketSlant's Analysis post the decision in June, 2016

SIFO IS KEY

Given the (lawsuits') failure both to explain why SIFO should track silver futures spreads, and to concretely plead that it did so consistently, a mere general correlation between these two is not sufficient to make SIFO a reliable benchmark such that deviations from it support a claim of irrational pricing animated by anticompetitive aims," Engelmayer wrote.

Analysis: a poor job was done explaining the role of SIFO in spread pricing.

SIFO represents the spread between expirations of FORWARD physical contracts in silver. The futures spread markets are derivative of the SIFO spreads. SIFO represents the cost-of-carry for physical silver and is used in determining lease/borrow rates over periods of time. These are in-turn extrapolated and the dominant factor in determining futures spreads on COMEX. Comex spreads are a direct function of SIFO. Without SIFO there are no spreads. And since SIFO was a much bigger market than the Comex spread market. The pricing mechanism was not fully transaparent. It was in the hands of a few dominant cartel-like players, as it had been for 30 years.

Analysis: The demand was fabricated

The market was only partially backwardated. Spot was below the next 6 expirations. Translation: there was no massive demand for immediate delivery. There was only demand in months where the last remaining floor traders who took risk trading their own money had positions. JPM's own book was likely short and had to get liquidity to cover their own positions. We knew Shak from our floor days, and were trading spreads off floor when this happened. They should not have lost this case. Comex traders do not trade spot. Spot was under the backwardation. Smoking gun? No, but damning circumstantial evidence in the least.

Bottom Line on the Trade

What really happened then was a silver miner had to hedge forward and cover up front. JPM likely had this client cornered and faded their back month bids. The miner, having no where else he could go, hit them OTC, when they were much better bid on the floor. Once SIFO and COMEX spreads are proven to be linked, the case will be made.

Blythe Did a Mini Buffet to a Client

How come in 1997 when Warren Buffet, who actually stood for delivery, the market did not rally until AFTER the spreads backwardated all the way to spot? Yet in 2011, the market had rallied already, and all of a sudden spreads (literally overnight during asian and london hours) went into backwardation? In a real market, the spread activity predicts the physical demand before the flat price does. You see the spot price start to act squirrelly to the front month future in the EFP. There are exceptions to this. But it is rare.

This trader also remembers that in 1997, Buffet was asked by the Govt to defer his request for delivery a year. He happily complied by selling spot and rolling out to a 1 year future. Payout? He netted an ROR of 40% due to negative carry without selling. Effectively he lent the producers their silver back to them ($7.40) at a premium of approximately 40% higher than his cost ($4.50). So Blythe did A mini Buffet, that's all.

Why wasn't that opportunity afforded SHAK and other locals? Does that have to be answered beyond this: In Mr. Buffet's case "the integrity of the market was at stake"( Hunt Brother's anyone?). The whole Silver mining industry was in jeopardy. (TBTF). But in Shak v.JPM only locals got burned. I'm sure each one of my arguments for manipulation can be taken apart by some lawyer or expert. But that is what they do. Facts against them? Argue the Law. Law against them? Argue the facts. Both against them? Use ad hominum attacks to shoot the messenger.

But for now it is fair to say "Based on information and evidence, we believe the Silver spread market was rigged your honor." And the Appeals court indeed, agreed that there was enough evidence to look further into this. Next comes the discovery and fact finding.

The sad part is, government is 20 years late. The US citizen has already been sheared for a generation losing billions. Banks have moved on to greener pastures. It is now safe to prosecute US buggy whip makers to mix a metaphor.

Read more by Soren K.Group