When you think of the top 1 percent of all income earners in American households, how much do you think this group rakes in? Millions? Tens of millions? What about the top 10 percent?

On the contrary, to be considered in the top 1 percent of taxpayers nationally, you’d need an annual income of $480,930. The top 10 percent of taxpayers make at least $138,031. These figures are based on 2015 income tax data, the most recent year available.

This income level varies widely by both state and city. In San Jose, California, the top 1 percent income threshold is close to $1.2 million, almost double the level for Los Angeles. As seen in the chart below, the spread is fairly wide between the top 10 most populous cities in the U.S. In San Antonio, Texas – home to U.S. Global Investors – you’d need to make $416,614 annually to be considered in the top 1 percent, slightly below the national threshold of top 1 percenters.

Earning enough income to be in the top 1, 10 or even 20 percent is no small accomplishment, but chances are good that many people you know, and may not think of as wealthy, fall into the top 1, 10 or 20 percent.

Is the Top 1 Percent Paying Their Fair Share?

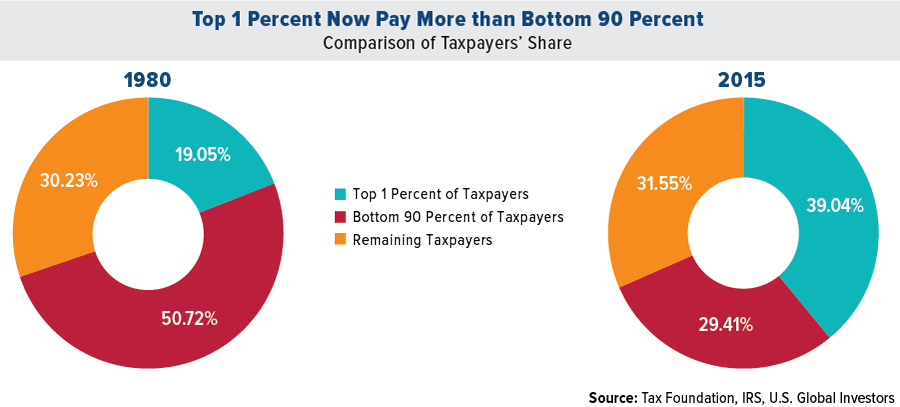

Contrast the above income statistics with the picture often painted in the media that the wealthiest Americans aren’t paying their fair share. According to the Tax Foundation, the top 1 percent of households collectively pay more in taxes than all of the tax-paying households in the bottom 90 percent.

Take a look at how much this has changed over the past few decades. In 1980, the bottom 90 percent of taxpayers paid about half of the taxes. The top 1 percent contributed about 20 percent. Now, the top 1 percent pays more than the bottom 90 percent. Perhaps this is more than their fair share?

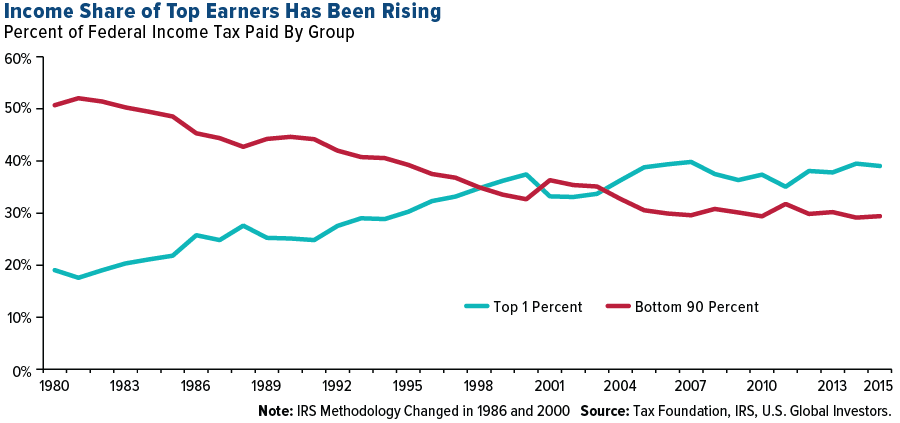

Below is the line chart from the Tax Foundation showing how the income tax share for each category has changed since 1980. For the majority of years, the share of the bottom 90 percent fell while the share of the top 1 percent rose.

Individual Tax Rate Cuts Take Effect in 2018

Taxpayers in the highest bracket should see a noticeable change when filing for the 2018 tax year since the top rate fell from 39.6 percent to 37 percent. President Donald Trump’s administration passed the Tax Cuts and Jobs Act in late 2017, which included small reductions to income tax rates for most individual brackets plus changes to exemptions, deductions and more. The average top 1 percent taxpayer will get a tax break of over $50,000 in 2019, according to estimates.

The new tax bill, however, eliminates the ability of taxpayers to deduct more than $10,000 in state and local taxes from their federal tax returns. This could significantly increase the tax burden of top earners who itemize their deductions in high-income tax states such as California and New York. One possible solution for these investors could be to take advantage of municipal bonds, which are often exempt from local, state and federal taxes.

Maximize Tax-Advantaged Investment Vehicles

Although it can be discouraging to see how top earners pay the majority of income taxes, there are still tax advantages for hard-working Americans who make saving and investing a priority in their lives.

How can you help make sure less of your money is going to the government and more of it is working for you in your investments? One way is to maximize your contributions to tax-advantaged investment vehicles such as an individual retirement plan, a 401(k), individual retirement account (IRA) or simplified employee pension (SEP) for the self-employed, all of which offer tremendous tax benefits.

To make it easier to have the discipline to set money aside, try an automatic plan that invests a fixed amount at regular intervals, such as the U.S. Global Investors’ ABC Investment Plan.

Wealth Isn’t Just a Number

No matter how much you earn, wealth is determined by how much you keep. My friend, Alexander Green, chief investment strategist of the Oxford Club, is a great source of inspiration for me and for many investors with his uplifting, holistic articles that relate to both health and wealth. Alex says wealth isn’t necessarily determined by an income figure. Instead, real wealth is determined by looking at your balance sheet. Here’s his formula:

“Maximize your income (by upgrading your education or job skills). Minimize your outgo (by living beneath your means). Religiously save the difference. (Easier said than done.) And follow proven investment principles.”

What matters most is being grateful for what you have. I’m a big believer that wealth is not a number or an amount, it’s an attitude and the umbilical cord to attitude is gratitude.

Take a look at my 10 favorite wealth and prosperity affirmations in this slideshow!

----------------------------

All opinions expressed and data provided are subject to change without notice. Some of these opinions may not be appropriate to every investor. By clicking the link(s) above, you will be directed to a third-party website(s). U.S. Global Investors does not endorse all information supplied by this/these website(s) and is not responsible for its/their content.

U.S. Global Investors, Inc. is an investment adviser registered with the Securities and Exchange Commission ("SEC"). This does not mean that we are sponsored, recommended, or approved by the SEC, or that our abilities or qualifications in any respect have been passed upon by the SEC or any officer of the SEC.

This commentary should not be considered a solicitation or offering of any investment product.

Certain materials in this commentary may contain dated information. The information provided was current at the time of publication.

Read more by Frank Holmes